Crypto is taxed when you sell it, trade it, spend it, or earn it. In most countries, including the US and UK, cryptocurrency is treated as property. This means you pay tax on profits when you dispose of them, and income tax when you receive them. In simple terms, crypto taxes apply when value is created or realized.

- Key Takeaways

- How Do Crypto Taxes Work?

- How Crypto as Property Works

- What Are Taxable Events in Crypto?

- What Is Capital Gains Tax?

- Is Moving Crypto in My Wallets Taxable?

- Do You Pay Taxes on Crypto Before Withdrawal?

- What is the Crypto Tax Rate?

- Can I Do My Crypto Taxes Alone?

- Consider Crypto Tax Software to Track Your Activity

- How Do Bitcoin Taxes Work?

- How Do Ethereum Taxes Work?

- Ways to Save on Your Crypto Taxes

- FAQs

- Conclusion

If you have bought Bitcoin, traded Solana, or earned rewards from Ethereum, you may already have taxable activity. Many people do not realize that even simple actions like swapping coins or paying with crypto can trigger a tax bill.

This guide breaks down:

- When crypto becomes taxable

- How your profit is calculated

- Simple ways to legally reduce what you owe

Key Takeaways

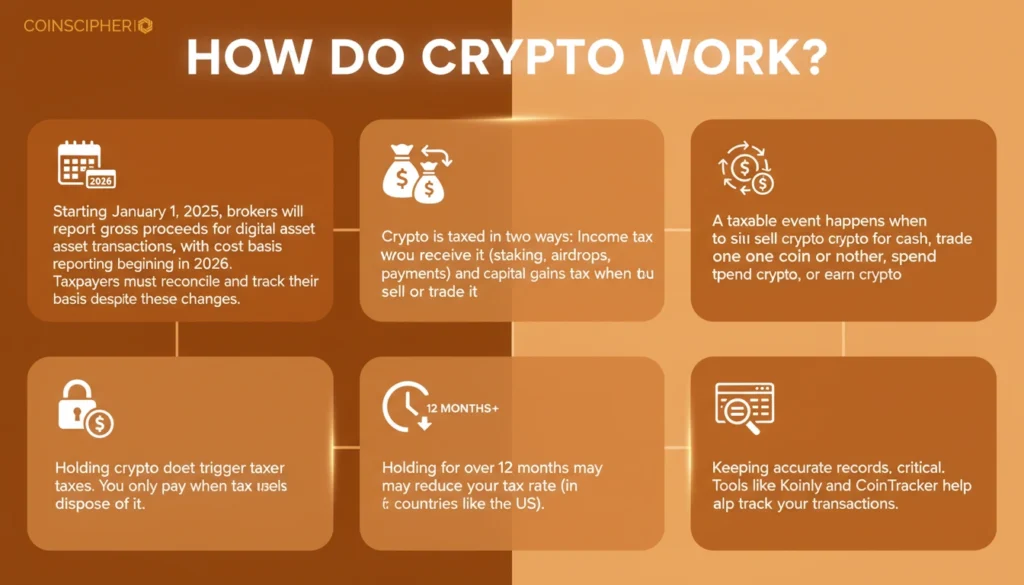

- Starting January 1, 2025, brokers will report gross proceeds for digital asset transactions, with cost basis reporting beginning in 2026. Taxpayers must reconcile and track their basis despite these changes.

- Crypto is taxed in two ways: Income tax when you receive it (staking, airdrops, payments) and capital gains tax when you sell or trade it.

- A taxable event happens when you sell crypto for cash, trade one coin for another, spend crypto, or earn crypto.

- Holding crypto does not trigger taxes. You only pay when you dispose of it.

- Holding for over 12 months may reduce your tax rate (in countries like the US).

- Keeping accurate records is critical. Tools like Koinly and CoinTracker help track your transactions.

How Do Crypto Taxes Work?

Crypto taxes work by applying income tax when crypto is received and capital gains tax when it is disposed of.

Crypto taxes are based on two main rules: income and capital gains.

- You pay income tax when you receive crypto, such as from staking, airdrops, or payments.

- You pay capital gains tax when you sell, trade, or spend crypto at a higher value than you acquired it.

Your profit is calculated as:

Sale price – purchase price = taxable gain

If you sell at a loss, you may be able to reduce your taxes.

How Crypto as Property Works

Most countries treat crypto like an asset, similar to stocks. Taxes apply when you sell crypto, trade it for another coin, or convert it to cash. The tax is based on your profit, which means the value when you sell it minus what you originally paid. If you earn crypto from staking, you may owe tax when you receive it and again if you later sell it for a higher price.

When the law is looking at crypto as property, it means that the taxes are triggered when you dispose of it, not just own it. Think of it like your piece of land or a share of Apple stock.

For example, you already know that your Apple stockbroker reports your transactions to your tax authority through Form 1099-B. Look at it similarly to crypto transactions, but now you will be getting Form 1099-DA (the name may vary by jurisdiction). So, if you spent a coin or traded or sold it on a custodial platform like Coinbase, the government will be expecting you to file returns.

The Wash Sale Rule in Crypto

Source: NTO

The wash sale rule currently does not apply to cryptocurrency in the United States. IRS rules for stocks prevent you from selling a losing investment to claim a tax deduction and then buying it back immediately (within 30 days). If you do this with a stock, the loss filling is disallowed.

However, as of early 2026, these rules generally do not apply to cryptocurrency. This is because it is classified as property rather than a “security” in this specific tax context. So, if your Bitcoin value drops, you can sell it, claim the capital loss to lower your tax bill, and buy it back minutes later at the same price.

What Are Taxable Events in Crypto?

A taxable event is a transaction that makes you liable for taxes. As I had explained earlier, not every transaction you carry out with crypto leads to a tax bill. The authorities will only come knocking if it leaves your possession or changes form. Sell crypto for fiat currency: e.g., exchange BTC for BBP, EUR, or USD.

The most common taxable events are:

- Selling crypto for fiat (USD, EUR, GBP)

- Trading one cryptocurrency for another

- Spending crypto on goods or services

- Receiving crypto as income (staking, airdrops, salary)

Non-Taxable Crypto Events

The following actions do not trigger a tax bill:

- Buying crypto with cash

- Transferring crypto between your own wallets

- Holding crypto without selling or using it

Not every crypto transaction creates a tax bill. The table below summarizes common taxable and non-taxable events:

| Activity | Taxable? | Why |

| Buying crypto with cash | No | You still own the asset |

| Selling crypto for cash | Yes | You realized a profit or loss |

| Trading BTC for ETH | Yes | BTC is treated as sold |

| Moving crypto to your wallet | No | Ownership didn’t change |

| Paying with crypto | Yes | It counts as disposing of the asset |

Crypto Investing Taxes (Buy, Sell, Hold)

If you use your hard-earned cash to buy a digital asset, wait for the market to move, and eventually sell it, you are investing. From the perspective of the tax agency, you are acquiring property and then disposing of it. You’ll get taxed on the capital gain, which is the difference between the cost of a digital currency and what you received at the end.

Here is an example. If you bought $100 worth of Solana and left it in your wallet for three years, you will owe nothing to the tax authorities. If the value increases to $200, you will pay taxes on the $100 value increase when you exchange coins for cash or use the value to buy another coin.

Crypto Income Taxes (Staking, Airdrops, Payments)

You could get extra crypto by staking to help secure the network or from an airdrop when a new coin is being launched. The mistake I have noticed is that many investors never consider this a taxable event. You should understand that in the eyes of the law, this is ordinary income. You will be taxed on the amount based on the market value at the time you received it.

Similarly, any crypto that you get as a payment for your effort, time, or services rendered is taxed as ordinary income. The tax bill is based on the fair market value at the time the coin becomes yours.

Here is an example: If you earn 0.1 ETH in staking rewards when ETH is worth $3,000, you have effectively earned $300 in income. You must report that $300 on your tax return for that year for income tax.

But here is where it gets even more twisted:

Suppose you let these earnings sit in your wallet for some time, during which the value grows from $300 to $500. If you later sell your ETH, the tax authority also expects you to file capital gains tax on the $200 profit gained. So, you will pay taxes for two things: the income you got from earnings and the profit you made when you sold the asset.

Crypto Spending Taxes (Using Crypto for Purchases)

Source: Solana Spaces

If you use crypto debit cards to buy items online or settle a bill, the tax office assumes you disposed of an asset and used the cash for purchases. The tax office will check if the crypto has grown in value since you first acquired it.

Think of this: you bought $100 worth of Bitcoin several years ago and used it to buy a $1,000 console today. You effectively made a $900 profit from that investment. Despite not cashing this money into a bank account, you still owe taxes on the value gain. However, if you deposited Bitcoin and used it immediately, you don’t owe any tax.

What Is Capital Gains Tax?

Capital gains tax is the tax you pay on the profit from selling or disposing of crypto.

As you may have seen in the examples above, any profits you make from your crypto are taxed at the time of selling your holdings. A profit is a gain in value from the time you received your crypto.

Here is how to calculate it:

Cost Basis = (Purchase Price of Crypto + Transaction Fees)

When you dispose of the crypto, you subtract the cost basis from the sale price.

Sale Price – Cost Basis = Capital Gain (or Loss)

For example, if you bought $4,000 worth of Bitcoin and paid $50 in exchange fees, your cost basis is $4,050. If you sell that Bitcoin later for $7,000, your taxable capital gain is $2,950.

Does it Matter How Long You Hold on to Your Crypto?

Yes, you can claim a lower tax if you have held onto your crypto for a longer period. Let me break this down into long-term and short-term capital gains.

- Short-Term Capital Gains: If you hold crypto for one year or less before selling or trading it, the profit is taxed at the same rate as your normal income. In the US, this can range from 10% to 37% depending on your total earnings.

- Long-Term Capital Gains: If you hold your crypto for more than one year (366 days or more), you qualify for much lower tax rates. In the US, these rates are usually 0%, 15%, or 20%.

Here is an example that can help you plan and actually pay a lower tax

You buy Bitcoin for $20,000. Six months later, you sell it for $30,000. You pay your income tax rate on the $10,000 profit. However, if you waited 13 months to sell it for $40,000, you would pay the long-term rate, which for many people is only 15%. See? You could end up paying a lower tax by holding your crypto longer.

Is Moving Crypto in My Wallets Taxable?

Moving crypto between your own wallets is not a taxable event.

You don’t get a tax bill for simply moving your crypto around. However, some movements may result in new wealth, which would actually be taxed. Let’s discuss some scenarios that differentiate between what is taxable and what is not.

Crypto Swaps (Trading One Coin for Another)

You may swap one coin for another to spend or earn a profit from a perceived value increase. A swap is regarded as two separate transactions by the tax authorities. The only difference is that both happen simultaneously.

Here is my favorite example: If you trade Bitcoin for Ethereum, the IRS will treat it as if you sold your Bitcoin at the current market value in cash and immediately used the cash to buy Ethereum.

Since you have disposed of your Bitcoin, any profit that you made while you held it is taxable. So, if you bought BTC for $500 and swapped it when it was $800, you owe capital gains tax on the $300 profit.

Transferring Crypto Between Your Own Wallets

Many crypto investors have more than one wallet. Let’s say such an investor moves crypto from an exchange to a hardware wallet like Ledger or Trezor. Or, simply move cash from one exchange to another. Doing so doesn’t trigger a tax event, as there is no change in ownership. So, no property disposal occurred.

Are Transfer Fees Taxable?

Wallets will normally charge you to move digital assets. The gas fee is definitely a cost attached to your coins. Since you are spending it to make the move, it is technically a disposal. While individual transfer fees are usually quite low, they may add up fast across the year. This may require you to calculate the tax owed.

My recommendation is to always keep records of your transfers so that you don’t lose the initial cost of your digital currency. Otherwise, the tax authority may see coins arriving as new income with $0 cost, which may cause you to overpay on taxes.

Airdrops and Hard Forks (Tax Treatment)

A hard fork is a case where a blockchain splits into two, like the Bitcoin/Bitcoin Cash split. Here, you find yourself owning a new type of coin. On the other hand, an accidental airdrop is when a project sends you tokens to your wallet as a reward or as a marketing move.

The tax agency treats the new cash as ordinary income the moment it gets to your wallet. This means that you are taxed on the fair market value of those coins on the day they are available to you. For example, if you find $200 worth of a new fork coin in your wallet, you will report it as income on your tax return.

However, if you sell those coins for $300, you will also pay a capital gains tax on the $100 profit. The same applies to the accidental airdrops.

Do You Pay Taxes on Crypto Before Withdrawal?

You do not pay taxes simply for withdrawing crypto to your bank account or another wallet. Taxes are triggered by taxable events, not by withdrawals themselves.

A withdrawal is only taxable if it involves a disposal of crypto. This includes selling crypto for cash, trading it for another asset, or using it for payments.

For example:

- If you sell crypto on an exchange and withdraw the cash to your bank account, the taxable event is the sale, not the withdrawal.

- If you transfer crypto between your own wallets, there is no tax because ownership does not change.

- If you convert crypto to fiat and withdraw it, you may owe tax on any profit made before the withdrawal.

What is the Crypto Tax Rate?

The crypto tax rate depends on your country, your total income, and the nature of the transaction. In the U.S., short-term gains are usually taxed at 10%–37%, and long-term gains at 0%, 15%, or 20%. At the top of this, high earners pay a 3.8% Net Investment Income Tax.

On the other hand, if you are an independent contractor, any crypto received as payment for services is also subject to self-employment tax.

If you live in the UK, capital gains are usually taxed at 18% or 24% (depending on your tax band). Any crypto earned through mining or salary is taxed as income at rates of 20%, 40%, or 45%. Other jurisdictions have different rates.

Can I Do My Crypto Taxes Alone?

Yes, you can calculate your crypto taxes yourself. However, this depends on your activity level. If you only bought Bitcoin once on Coinbase and sold it a year later, the math is simple.

But if you trade across multiple exchanges, move coins to hardware wallets, and participate in DeFi or NFT minting, doing it manually is nearly impossible. This is because you have to track the “fair market value” in your local currency for every single transaction at the exact time it happened.

Consider Crypto Tax Software to Track Your Activity

Crypto tax software documents all your tax events, especially when you are dealing with several cryptocurrencies, wallets, or transactions across the year. If you are an international trader who pays and moves crypto across different countries, pick a tool that has a clean interface and tracks crypto transactions across multiple jurisdictions. Koinly is a good choice as it tracks crypto activity across countries like the UK, Canada, and Australia.

However, if your primary crypto liquidity flows through major US exchanges like Coinbase or Kraken, consider Cointracker. It offers a ‘one-click’ workflow to TurboTax and H&R Block and populates your IRS Form 8949 automatically.

How Do Bitcoin Taxes Work?

Bitcoin taxes follow the property rule. You only pay taxes when you dispose of your crypto. Here is an example: if you buy 0.5 BTC for $20,000 and sell it for $25,000, you owe tax on the $5,000 gain.

On the other hand, if you use Bitcoin to buy a $60,000 car, and that Bitcoin originally cost you $10,000, you owe capital gains tax on $50,000, even though no cash changed hands.

How Do Ethereum Taxes Work?

Ethereum taxes are similar to Bitcoin taxes for simple buys and sells. However, there are new taxes for staking. If you stake ETH, the rewards are taxed as income based on their value on the day you receive them.

Ways to Save on Your Crypto Taxes

There are several ways to cut your tax bill. Given that the tax agency charges when you make a profit or gain from existing assets, you can always lower taxes by looking at these areas. Here are a few ways to go about that.

Sell Losing Assets (Tax-Loss Harvesting)

Suppose you bought two batches of Bitcoin at different times. The first batch gives you a profit of $1,000, while the second one has dropped by a similar amount; you could save on taxes by cancelling the loss.

This is how to go about it: sell the losing asset to realize the loss. This means that the loss has cancelled out the profit, leaving you with no taxes.

Check the maximum allowed amount you can recover from your taxes in your jurisdiction. Also, weigh whether offsetting a loss is more advantageous than waiting out the losing asset to gain value.

Gifting and Donating

You may also give crypto or donate it to a charity. The amount you can gift varies from one country to another. The person receiving the gifts inherits the original cost basis of the token.

Remember, if you donate crypto you have held for more than a year, you will not be charged capital gains taxes. You can also claim a tax deduction for the full fair market value of the donation, thereby lowering your taxes on regular income.

FAQs

-

Do I have to pay taxes on crypto if I didn’t sell it?

No. You only pay taxes when you sell crypto.

-

How much capital gains will I pay on $200,000?

It depends on your income and how long you have held your crypto. If you held it over a year and are in the 15% long-term capital gains bracket, you’d pay $30,000. However, you could pay up to $74,000 (37%) in the US if you held it for a shorter period.

-

What records should I keep for crypto taxes?

Record the date you received crypto, the buying price, the date of sale, and the selling value.

-

Is trading one crypto for another a taxable event?

Yes. When you swap BTC for ETH, you sell BTC and purchase ETH. You owe tax on any profit made on the BTC.

-

Are staking rewards taxable?

Yes, you pay tax on ordinary income at its fair market value on the day you receive it.

-

Do crypto exchanges send tax forms?

Yes, starting in 2026, exchanges will issue Form 1099-DA in the US. It reports your transactions to both you and the IRS.

-

Do I have to report crypto tax if I made a loss?

Yes, report a loss to avoid penalties. You can lower your overall tax bill by offsetting other gains you made in the year.

-

Can tax authorities see my crypto transactions?

Yes. Major exchanges share data with tax agencies. So, your crypto movement is tracked.

-

What happens if I don’t report crypto taxes?

You can be required to pay interest, stiff financial penalties, and in extreme cases, face criminal charges.

-

Does the wash-sale rule apply to crypto?

As of early 2026, the wash sale rule does not apply to crypto in the US. So, you can sell at a loss and buy back immediately.

-

What tools help track crypto gains and losses?

Tools like Koinly and CoinTracker aggregate data across wallets.

-

Is transferring crypto between my own wallets taxable?

No. Moving assets from one wallet to another is not a taxable event because ownership hasn’t changed.

-

Is withdrawing crypto from an exchange taxable?

It depends. If your crypto has gained value, you will pay capital gains tax. The fee may also attract taxes.

Conclusion

You will no longer be able to hide your crypto transactions from the tax authorities. You better learn what attracts a crypto tax bill and what does not. From our discussions, any increase in value for your crypto attracts a tax bill when disposing of it.

Going forward, keep your crypto records accurate. Take advantage of discounts, donations, and tax-loss harvesting advantages to lower your tax bill. Also, check out which tools can help you keep records so you can focus on the next move in the marketplace.

I’m Eric Nkando, a crypto and crypto tax enthusiast, with other extensive experiences in forex and stock markets. I believe crypto and blockchain are no longer alien topics and I’m here to help investors tackle emerging issues of taxation and prudential investment strategies. My approach? Delivering clear, insightful analysis on digital assets, market trends, and trading strategies, bridging complex technical concepts with practical investment perspectives. My work has been widely published on leading financial platforms such as Investing.com, FXLeaders, and The Distributed.